Breaking it Down: Let's have a conversation about the 1933 Gold Seizure.

Welcome to 'Breaking It Down,' where we embark on an enlightening journey into the world of futures, commodities, bonds, equities and more! In this edition, we shift our spotlight to the gold seizure.

The 1933 gold seizure in the United States was a significant event in the country's economic history.

Background - Economic Crisis and Gold Standard Abandonment:

The Great Depression had severely impacted the U.S. economy, leading to widespread unemployment and financial instability.

To supposedly combat the economic crisis(wink wink say no more, take my gold Mr. President), President Franklin D. Roosevelt took office in 1933 with a promise to implement bold measures.

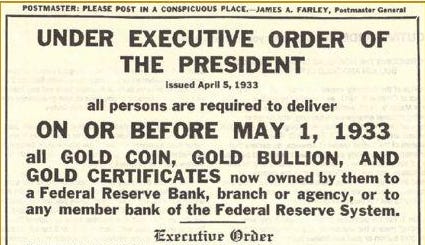

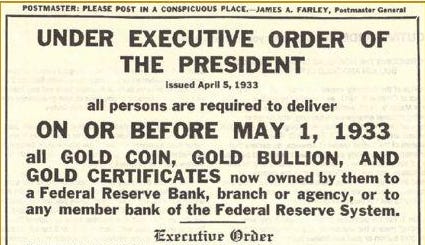

Executive Order 6102 - Gold Confiscation:

On April 5, 1933, President Roosevelt issued Executive Order 6102, which prohibited the hoarding of gold coins, gold bullion, and gold certificates by U.S. citizens.

The order required individuals to exchange their gold holdings for U.S. dollars at a fixed rate of $20.67 per ounce.

Gold Reserve Act of 1934:

The Gold Reserve Act of 1934 followed Executive Order 6102 and was signed into law on January 30, 1934.

This act further solidified the government's control over gold, effectively ending the gold standard in the United States.

The act raised the official price of gold to $35 per ounce, which provided the government with a substantial profit as it had acquired gold at the lower rate under Executive Order 6102. Call it QE -1.

Rationale for Seizure:

The government's insane rationale was to stimulate economic recovery during the Great Depression. By confiscating and controlling gold, it aimed to increase the money supply and encourage spending and investment. Through theft of their citizens. (Spending at gunpoint)

Impact on Citizens:

Many individuals and businesses had to surrender their gold holdings to the government. Those who didn't comply faced penalties, including fines and imprisonment.

The seizure was initially met with resistance by some citizens who opposed the government's interference in private property rights.

Side note: Numerous individuals and businesses faced legal action as a result of Executive Order 6102, but some of these cases saw creative defense strategies. In one instance, a New York lawyer named Frederick Barber Campbell was prosecuted. However, Federal Judge John M. Woolsey declared the prosecution invalid because the order was signed by the President, not the Secretary of the Treasury as required by law. Campbell had a substantial deposit of over 5,000 ounces of gold at Chase National Bank. When he attempted to withdraw his gold, the bank refused, leading Campbell to file a lawsuit against Chase. Shortly after, a federal prosecutor charged Campbell for failing to surrender his gold. Despite the unsuccessful prosecution of Campbell, the federal government managed to seize his gold. This case prompted the Roosevelt administration to issue a new order, bearing the signature of the Secretary of the Treasury, Henry Morgenthau, Jr.

Abandonment of the Gold Standard:

The 1933 gold seizure effectively ended the gold standard in the United States. The country shifted from a gold-backed currency to a fiat currency system.

This allowed the government greater flexibility in managing the money supply and implementing monetary policy as they see fit.

Economic Effects:

It had the effect of devaluing the U.S. dollar in international markets, which made U.S. exports more competitive. Yeah…

Legacy:

The legacy of the 1933 gold seizure is a complex one. Nowadays, there's no need for anyone to steal your gold to reduce the value of your currency. Instead, it's a process that happens routinely.

The 1933 gold seizure was a significant event in U.S. history that marked the end of the gold standard. The Gold Reserve Act of 1934 gave the President the authority to determine the value of the U.S. dollar in terms of gold. Right after this law was passed, President Roosevelt changed the official price of gold from $20.67 to $35 per ounce. This essentially reduced the value of the U.S. dollar since it was tied to gold at that rate. This new gold price remained in place until August 15, 1971, when President Richard Nixon made a historic announcement. (Google: Nixon Shock) He declared that the United States would no longer guarantee to exchange its dollars for a fixed amount of gold, effectively abandoning the gold standard for international currency exchange.

The restrictions on private ownership of gold in the United States were lifted later on. President Gerald Ford signed a bill allowing U.S. citizens to buy, own, sell, or otherwise deal with gold both inside and outside the country. This change in the law took effect on December 31, 1974.

Jason Perz/AAO Research