The Dollar's Problem

For the last few weeks, investors have been asking whether the recent dollar strength marks the beginning of a larger move higher.

Maybe.

But if we’re going to get a sustained bull market in the dollar, one thing probably needs to happen first.

The short end of the yield curve has to start outperforming the long end.

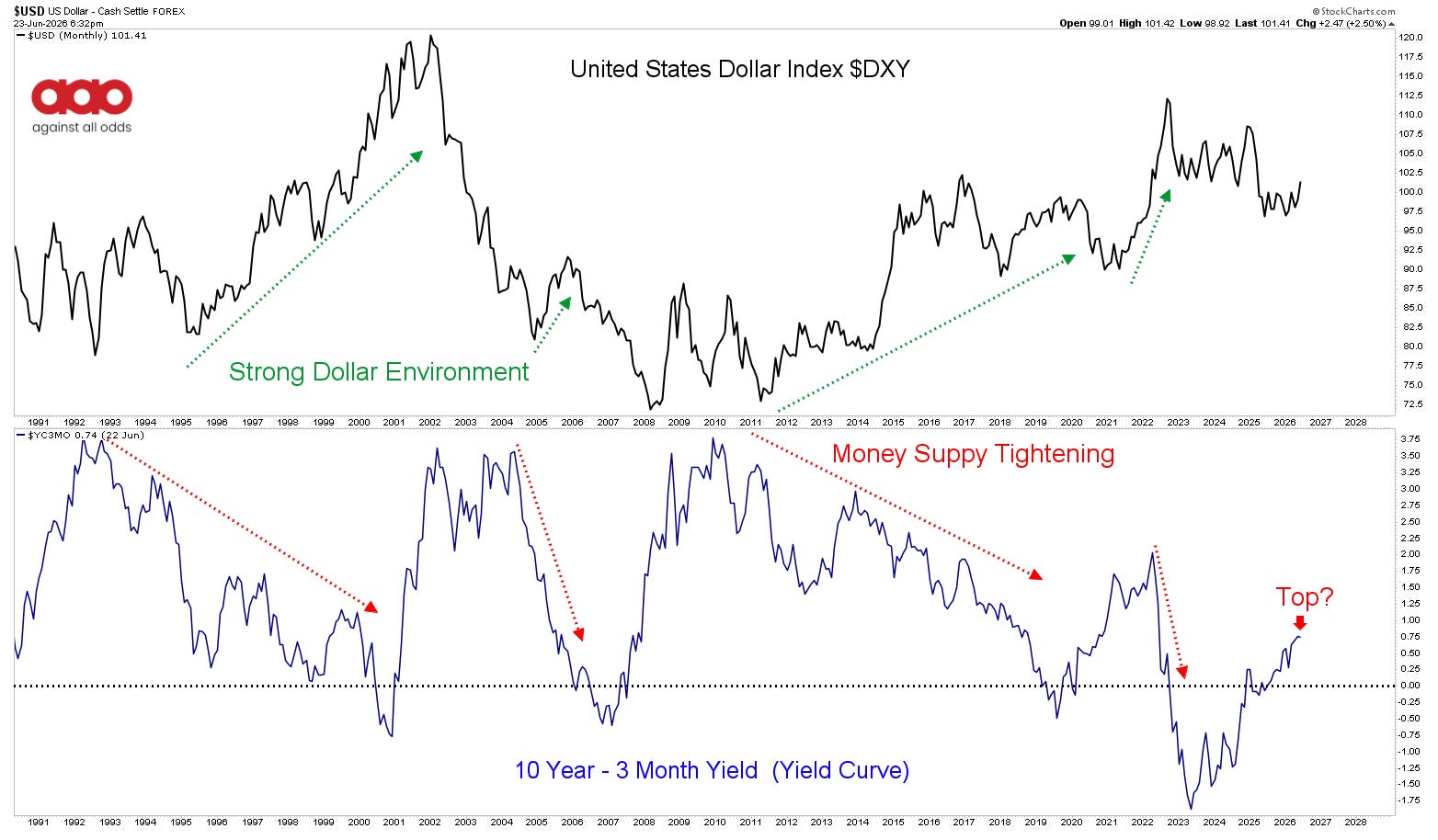

Take a look at the chart.

Historically, strong dollar environments have often coincided with periods where monetary policy was becoming tighter or liquidity conditions were becoming less abundant. That’s why I’ve paired the Dollar Index with the 10-Year minus 3-Month yield spread.

Notice what happens during many of the major dollar advances.

The yield curve tends to flatten or invert as the short end rises relative to the long end.

Why?

Because if the Fed is truly serious about fighting inflation, they need to raise short-term rates aggressively enough to tighten financial conditions.

And if they do that, the dollar tends to benefit.

That’s the bullish dollar argument.

The problem is that I think it’s a stretch.

Could the Fed raise rates again?

Sure.

Anything is possible.

But let’s be honest about what central banks are.

They are inflationary institutions.

They always have been.

The Fed talks about controlling inflation, but they never want zero inflation. They never want a shrinking money supply. Their entire framework is built around maintaining positive inflation over time.

That’s not a criticism. It’s simply how the system is designed.

The market seems to understand this.

Despite all the tough talk, the long end of the Treasury market has remained stubbornly elevated while the short end has not shown the kind of sustained leadership you would expect if a major tightening cycle were right around the corner.

That’s why this chart matters.

If the yield curve continues to steepen and long rates continue to rise relative to short rates, it becomes harder to make the case for a structurally stronger dollar.

If the short end suddenly starts outperforming and the curve begins flattening again, that’s a different conversation.

For now, I’m watching.

The dollar is trying to break out.

The Fed is trying to sound tough.

But price hasn’t fully confirmed the story yet.

As always, opinions are interesting.

The chart is what pays us.

The dollar. The yield curve. Bonds. Commodities.

These aren’t separate stories. They’re all connected.

At Against All Odds Research, we help investors connect the dots between macro trends and portfolio opportunities before the crowd catches on.

Join us and get access to our portfolios, trade alerts, weekly reports, and macro musings.

Against All Odds Research

Stay Connected:

YouTube: Against All Odds Research Channel (@againstalloddsresearch)

Twitter: Jason P (@jasonp138)

Substack: AAO Research

Support the Bees: Help save the native bees! Learn more and get involved here.

Thank you for repeating & explaining this for us. It's not necessarily a hard concept to comprehend but grasping the correlation & what it means is not exactly easy because the information is still fairly new.