The Most Dangerous Signal Is Relief

Inflation expectations are collapsing. History says that’s when policy mistakes begin.

“It is not things themselves that disturb us, but our opinions about them.” — Epictetus

Inflation hasn’t disappeared—it’s just been forgotten.

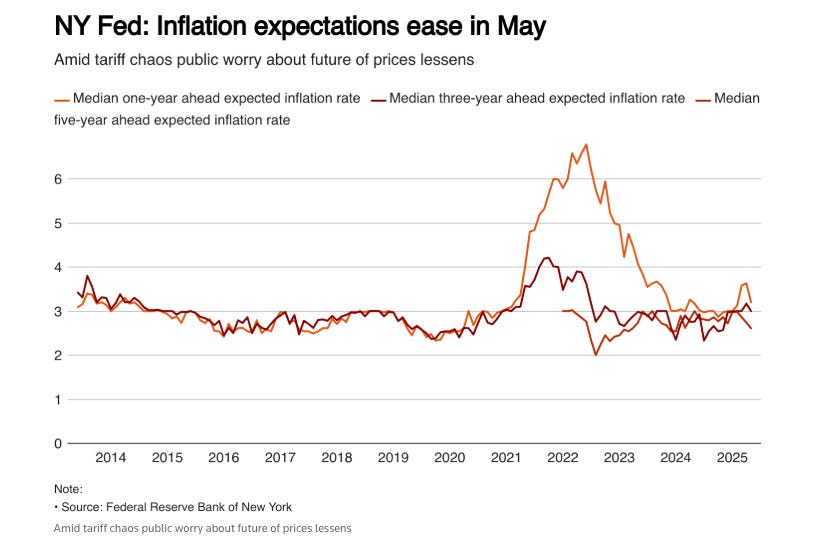

For the first time since 2024, inflation expectations fell across all major horizons in the NY Fed survey. One year projections dropped 0.4%, three year dipped 0.2%, and five year ticked lower to 2.6%. Confidence is rising, fear is fading and even credit stress is retreating.

That’s exactly what makes this dangerous.

Epictetus warned us: it’s not reality that disturbs us, it’s our perception of it.

Today, the perception is that inflation is behind us.

That price pressures have normalized.

That rate cuts are safe.

But if the Fed acts on that perception and cuts into rising commodity prices, a stabilizing labor market, and surging global equities—they risk reigniting the very inflation they believe they’ve conquered.

The lesson isn’t new—the second wave always comes after the fear dies.

In the 1970s, inflation surged again after policymakers prematurely eased.

In 2020–2021, trillions in stimulus were unleashed and led to the highest inflation rates that the market had seen in decades.

And now, with expectations back to 2.6%, we’re flirting with the same mistake—again.

If the Fed sees these surveys as clearance to cut, they’re no longer fighting inflation—they’re fueling it.

The market isn’t disturbed by inflation.

But as Epictetus might remind us, it’s not the event that matters. It’s our interpretation that does the damage.