The Rise of Agricultural Commodities: An Exclusive Commodity Report

Oil, Gasoline, Gold, Cattle, Cocoa... Got to catch them all! Welcome to our exclusive report.

In recent developments, we've observed signs of increasing demand across a wide range of commodity markets. This shift can be attributed to various factors, including rising export statistics, notable activity in bull futures spreads (with nearby prices outperforming deferred ones), strengthening cash basis levels (where cash prices surpass futures prices), and price index increases. These indicators suggest a potential turnaround in the U.S. and global economy, hinting at the possibility of a resurgence in consumer demand. This could mark a departure from the previous pessimistic outlook that commodities would experience a prolonged period of low demand.

Currently, funds have taken substantial short positions in what was deemed we will never see demand again in the commodity market. However, it appears that the extreme apathy towards demand may have been overstated. It might be time for a correction in the commodity market, leading to an upside rebalancing.

We hold a bullish outlook on commodities as we head later in to this year. Stay tuned for further updates and opportunities in this evolving market landscape.

Let’s get in to it.

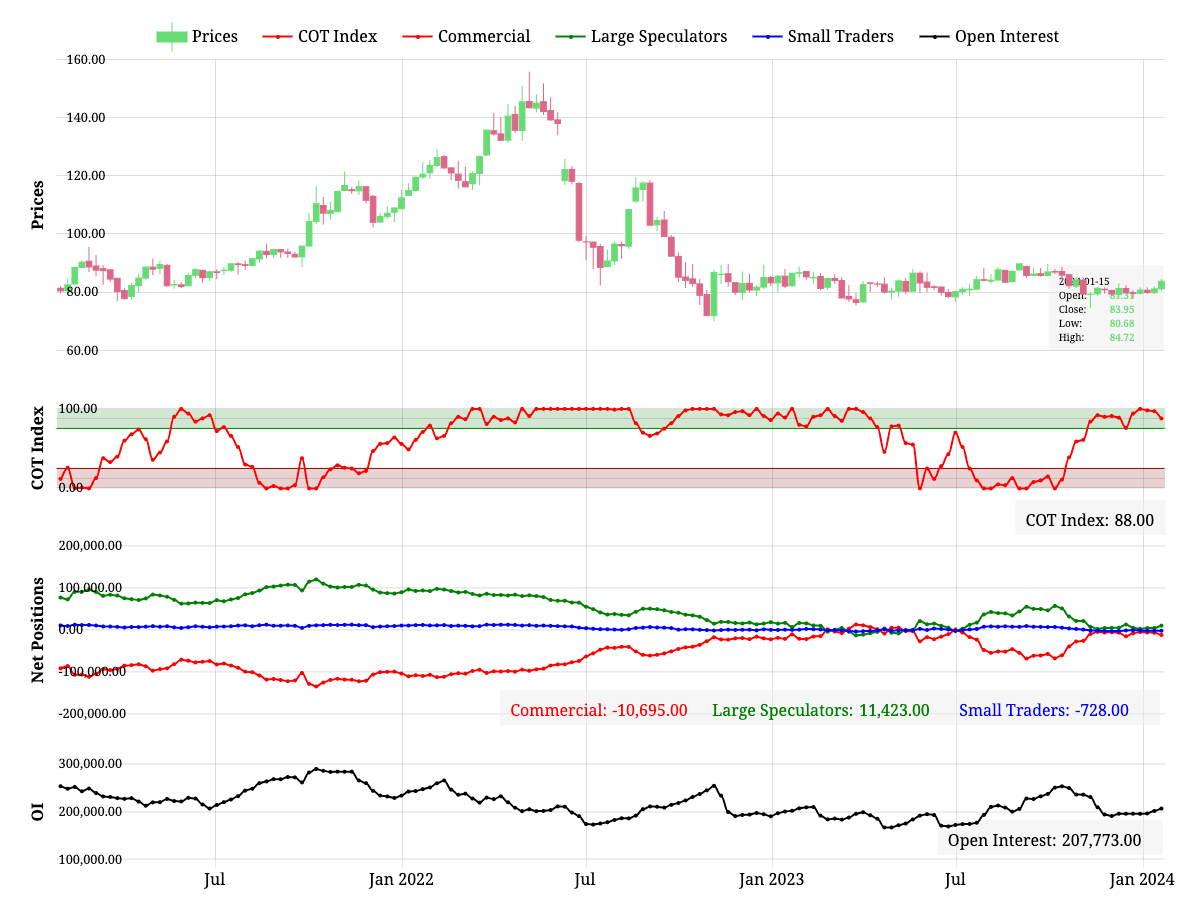

Cotton-Our new long trade, let’s dive in.

One noteworthy example of apathy in the commodities market is cotton, which has recently experienced a buy signal due to unexpectedly strong export demand. This could signal the beginning of a trend where speculators start covering their short positions, potentially allowing producers to make profitable cash sales and shield themselves from downward price risks. This proactive approach contrasts with the previous reactive stance driven by emotional fear.

With US cotton ending stocks currently at their lowest levels in nearly a decade, one might assume that poor export demand is the prevailing narrative. However, recent surprises in demand have the potential to disrupt this notion, prompting a shift away from the "no demand" perspective and the necessity to decrease ending stocks in the US, which could reach perilously low levels.

Notably, Chinese cotton prices are on the rise, reaching new highs, and cotton bull spreads are showing signs of a strong surge, indicating an increase in demand and the likelihood of tighter US balance sheets in the near future.

We see the recent cotton breakout as a harbinger of similar trends in grain and livestock markets, where the prevailing "no demand" narrative and extreme speculator short positions have become overcrowded trades.

For producers seeking to make cash sales, targeting the $0.89 cent range appears to be a strategic choice. Many producers have succumbed to panic selling during recent downward market movements in various agricultural sectors. However, a more prudent approach is to sell during rallies, when economic conditions are considerably more favorable for cotton prices. This approach offers a better opportunity to maximize returns.

The US dollar-The most important part of global macro at the moment.

Discussing the current economic landscape and its relevance to the US dollar, let's break it down:

Our market broad stock market signals are still incredibly bullish. Current lagging fundamental indicators show a low probability of such a recession materializing at this point. Internationally, the UK and Brazil seem to be displaying the most promising growth dynamics. None of this will put too much pressure on the dollar either way.

The Federal Reserve has undertaken a dovish pivot and the market is starting to price in rate cuts in the near term. Additionally, we anticipate that the balance sheet roll-off will continue over the medium term. To counterbalance this, the Treasury is expected to offset balance sheet roll-off through its low-net-bond-supply financing regime until the Reverse Repurchase Program balance is significantly depleted. This decrease in the RRP contributes to increased USD liquidity and aligns with the trend of rising global liquidity. While fiscal policy played a significant role in driving upside surprises in US growth in recent quarters, it is unlikely to remain as supportive over the medium term.

”Michael Feroli, the J.P. Morgan chief economist, was quoted in The New York Times using “immaculate disinflation” the next month.” Embarassing…