The Seven Day Scope (Snipers Only)

Weekly report showing you the current trends.

USD-Despite the re acceleration of US data and an increase in US yields, the DXY has failed to rally out of this range. Nonetheless, at AAO we perceive the possibility of the DXY moving higher compared to risk-sensitive currencies, mainly due to prevailing geopolitical uncertainties. The latest US data not only surpassed expectations but also indicate a re-acceleration, particularly in core and core-core services inflation. Additionally, non-farm payrolls (NFP) have shown signs of re-acceleration, accompanied by positive revisions. If the dollar can not rally here… I am not sure if it will. (We have closed our shorts in currencies against the dollar. Sitting flat for the moment) From issue:

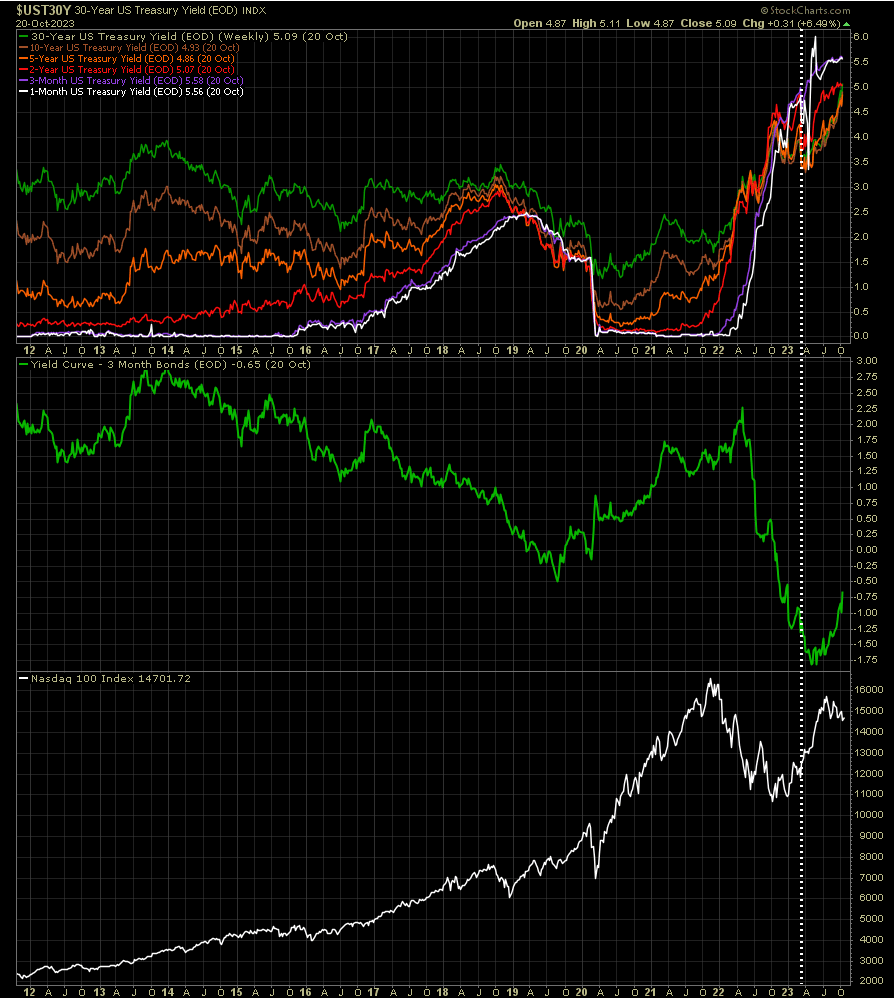

Yields-The increase in Treasury yields has triggered additional consequences. This surge has notably led to a considerable tightening of financial conditions, a change that was measured by the Morgan Stanley Financial Conditions Index (MSFCI). According to the latest data as of October 20, the conditions have tightened by an amount roughly equivalent to slightly over three 25 basis point hikes in the policy rate since the September FOMC meeting.