When Bond Markets Break, Inflation Follows

The BOJ lost control of the long end. What happens next won’t stay in Japan.

Yes, the U.S. just had a terrible 20-year auction. 30-year yields nearly retested the October highs from last year as we hit 5.15% this week.

But that’s not the real story…

The real bond crisis is in Japan.

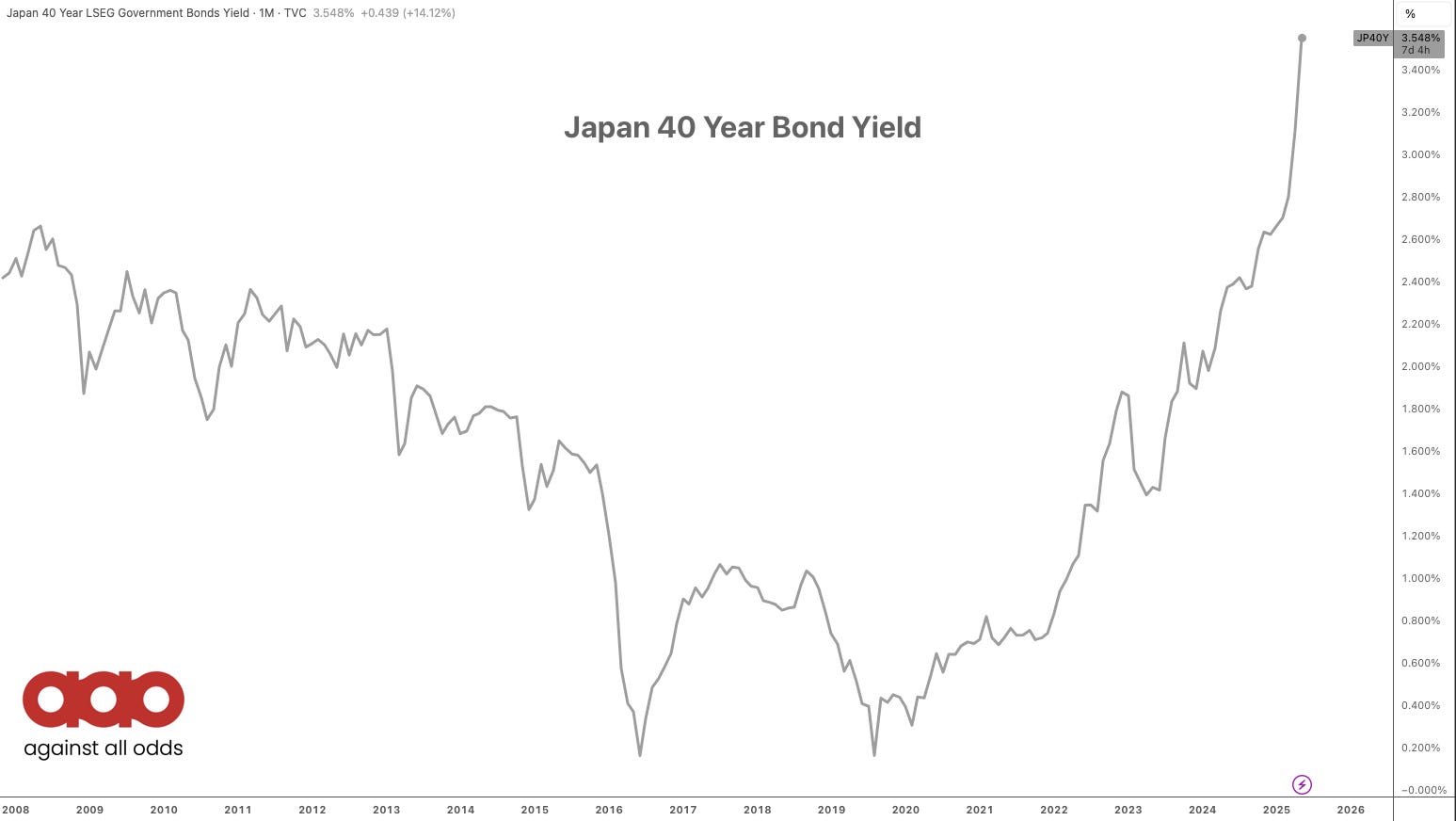

This week, Japan had its worst 20-year auction since 1987. Long-end JGB yields—30s and 40s—are ripping to all time highs.

Not because of growth or inflation. Because there are no buyers.

Life insurers, once the cornerstone of long-duration demand, are out. Their duration gap has flipped negative. New solvency rules have killed appetite, especially for the 40-year. The reinsurance complex is offloading JGBs. Past buyers are now net sellers. The market is overwhelmed with supply—and the demand side is structurally broken.

Add fiscal stress, political risk, and an upcoming election where tax cuts are being promised, and the bond vigilantes are wide awake.

This isn’t a local glitch, it’s bleeding into global markets.

Goldman says Japan’s 30-year move has already added 80 basis points of pressure to G4 long-end yields. That means what’s happening in U.S. Treasuries isn’t just about the Fed or the auctions—it’s ripple effects from Japan’s purge.

And this market isn’t liquid. The BOJ owns over half of the JGB market. When it breaks, it breaks hard—air pockets, no bids, and extreme volatility in long-dated swaptions. (See the bottom of this post for a quick lesson on swaptions)

Unlike in the U.S., there’s been no broad flight-to-safety. No stock drawdown. No yen break out (yet). Just a clean repricing of risk in the most critical part of Japan’s curve.

So what now?

Maybe the BOJ steps in—tweaks QT, boosts long-end purchases, talks up market stability. But unless there’s a major policy pivot, the selloff won’t stop. The underlying issue—too much supply, not enough demand—isn’t going away.

This is bigger than Japan.

Rising inflation, ballooning deficits, and collapsing duration demand are hitting every major bond market. Japan just happens to be first.

When the quietest central bank on Earth starts losing control of its bond market... that’s not background noise.

That’s the alarm bell.

When bond markets break, governments don’t stop spending—they just pay more to borrow. (Inflation)

That’s the inflation risk.

Japan’s long-end selloff is a canary in the coal mine. There’s too much debt, too little demand for duration, and central banks that are slowly stepping away. That dynamic doesn’t just raise interest rates—it raises the cost of funding governments addicted to deficits.

So what happens when borrowing gets more expensive?

They don’t cut spending. They issue more debt at higher yields.

And when a country like Japan—where deflation has been the default for decades—starts pricing in sustained inflation and rising yields, it’s a warning for the rest of the world: the era of cheap money is ending.

Higher bond yields force risk premiums up, debt costs up, and eventually prices up. Because if the cost of funding public services, entitlements, and industrial policy rises, it flows straight into the real economy.

That’s not a theoretical risk—it’s already happening.

And it’s not just Japan. The U.S., the UK, Europe—they’re all facing the same structural problem: massive deficits, aging populations, and less demand for their paper. Japan’s bond market just cracked first.

When debt issuance rises and buyers disappear, the central bank eventually has to step in—either openly or quietly.

And when they do?

Monetary policy loses credibility. Inflation expectations get unanchored. And suddenly, what used to be “transitory” becomes persistent.

So yeah—bond market dysfunction doesn’t just lead to volatility.

It leads to inflation.

Because when nobody wants your bonds… you print.

And when you print into a supply-constrained world… prices go up.

Every. Time.

Why I'm Still Long Japan

Everyone panicked. Yields spiked. The Japanese bond market buckled. And the narrative flipped: “Japan is uninvestable.”

But here’s the thing—price didn’t break. It shook out the weak hands... and then ripped higher.

Look at the chart.

$EWJ didn’t collapse. It didn’t trend lower. It staged one of the cleanest shakeouts you’ll see—flushing just enough fear to reset positioning—and then reclaimed the highs. That’s not bearish. That’s bullish.

Markets have a way of ignoring even the loudest headlines when the path of least resistance is up. Everyone was screaming about a JGB crisis. The yen was supposed to explode. Stocks were supposed to tank.

Didn’t happen.

That’s the tell. When the worst-case narrative is front and center—and price still breaks out—you respect it.

This is classic behavior at the end of a long base. The last fake-out before a real move. Japan’s been coiling for months. Now it’s breaking out while the rest of the world wrestles with slowing growth and sticky inflation.

Fundamentals matter—until they don’t. Price is the final arbiter.

And $EWJ just cleared multi-year resistance with authority.

So yeah, I’m still long Japan even though I know that this is a problem.

Because when everyone’s looking for reasons to sell—and price doesn’t flinch—that’s usually your trade.

🏆 Top Performers from Our Recent Reports:

Junior Gold Miners (GDXJ): +47.69%

Gold Miners (GDX): +45.81%

Colombia (GXG): +27.43%

Poland (EPOL): +45.29%

Japan (EWJ): +8.2% (If you are curious)

Germany (DAX): +31.8%

Copper (HG1): +16.47%

Bitcoin: +17.06%

What’s a Swap?

An interest rate swap is an agreement between two parties to exchange one stream of interest payments for another, typically:

Fixed rate ↔ Floating rate (like SOFR or LIBOR)

This helps institutions manage interest rate risk.

What’s a Swaption?

A swaption is an option to enter into that swap later.

You’re not committing to the swap today—you’re buying the right to do it in the future if it’s favorable.

📈 Want the trades before the breakout?

I share every position I’m in. Full transparency. Clear signals. No hindsight fluff.

Sign up for Against All Odds Research and get:

✅ Real-time trade alerts

✅ Weekly portfolio breakdowns

✅ Macro analysis that cuts through the noise

✅ Price-driven signals, not opinions

We caught Gold before the ramp higher buying it in 2023. We bought bitcoin before the break out to new all time highs.

You never know where the next winner will come from—but you can be ready for it.

👉 Join us here.

Against All Odds Research

Stay Connected:

YouTube: Against All Odds Research Channel (@againstalloddsresearch)

Twitter: Jason P (@jasonp138)

Substack: AAO Research

Support the Bees: Help save the native bees! Learn more and get involved here.

Brilliant one Jason.

5 years ago, if you told people that one day Japanese yields would spike, they would have called you crazy!

Just shows that when regimes change, they can change FAST